While Plan F isn't being discontinued, it won't be available to people who are newly eligible for Medicare after January 1, 2020.

As a senior market insurance agent, your clients will be looking to you for guidance and expertise as this change takes place. Are you prepared?

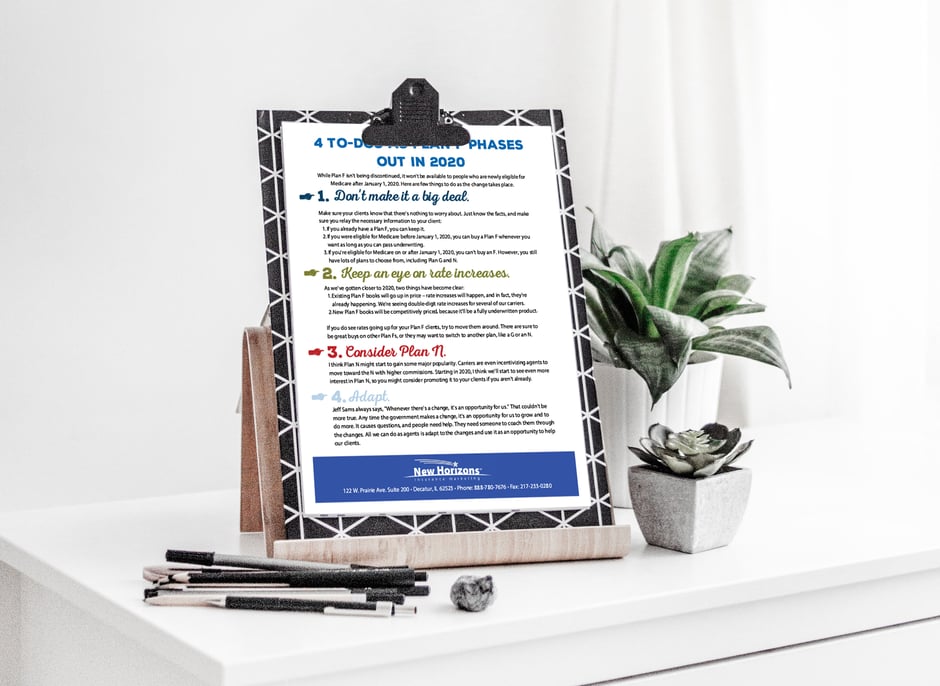

We've put together a quick to-do list with 4 pieces of advice that'll help you take great care of your clients.

What's Happening With Plan F in 2020?

This download gives you advice, but it doesn't outline the specific changes taking place. If you're not fully aware of the 2020 Plan F change, here's the scoop:

Congress first signed MACRA, the Medicare Access and CHIP Reauthorization Act of 2015. This massive piece of legislation covers a lot of ground, but what we're particularly interested in is Section 401:

Amends SSAct title XVIII to deny Medigap policies that cover Part B deductibles to Medicare beneficiaries newly eligible on or after January 1, 2020.

This means is that Medigap Plan F, High-Deductible F, and C can't be sold to newly eligible Medicare beneficiaries as of January 1, 2020.

You're considered newly eligible if you've attained age 65 or first became eligible for Medicare due to age, disability, or ESRD on or after January 1, 2020.

Plans D, G, and High-Deductible G (new) will be guaranteed issue plans for newly eligible Medicare beneficiaries.

Current enrollees who have Plan C, F, or High F can keep their plan.They can even continue to buy these after January 1, 2020 – they just have to pass underwriting.

Read the Full Plan F Is Phasing Out Article

This download is a shortened up, on-the-go version of our more detailed article, 4 Things Agents Should Do As Medigap Plan F Phases Out in 2020.

Be sure to read that article in full if you want even more information than what's available in this handout.

Download Now

Medicare has neither reviewed nor endorsed this information. Not connected with or endorsed by the United States government or the federal Medicare program.